A roof replacement is one of the largest home improvement decisions you’ll make — and in the NC Triad, where our seasons swing from humid summers to ice storms and the occasional severe hail event, it’s rarely a decision that arrives at a convenient time. Whether a storm just pushed the issue to the top of your list or you’ve been watching an aging roof and planning ahead, the question of how to pay for it deserves a lot more honest attention than most of what you’ll find online.

Most roofing financing content follows a predictable script: here are your loan options, here’s how to apply, here’s why our preferred lender is great. That script isn’t wrong, exactly — but it skips over the questions that actually matter to a homeowner who wants to protect both their home and their financial position.

This guide is different. We’re going to cover the full picture — the financing options themselves, yes, but also the decision sequencing that affects your negotiating leverage, how insurance claims and financing interact in ways that can cost you real money if you’re not careful, and why matching your loan term to your roof’s expected lifespan is a concept no one else seems to be talking about.

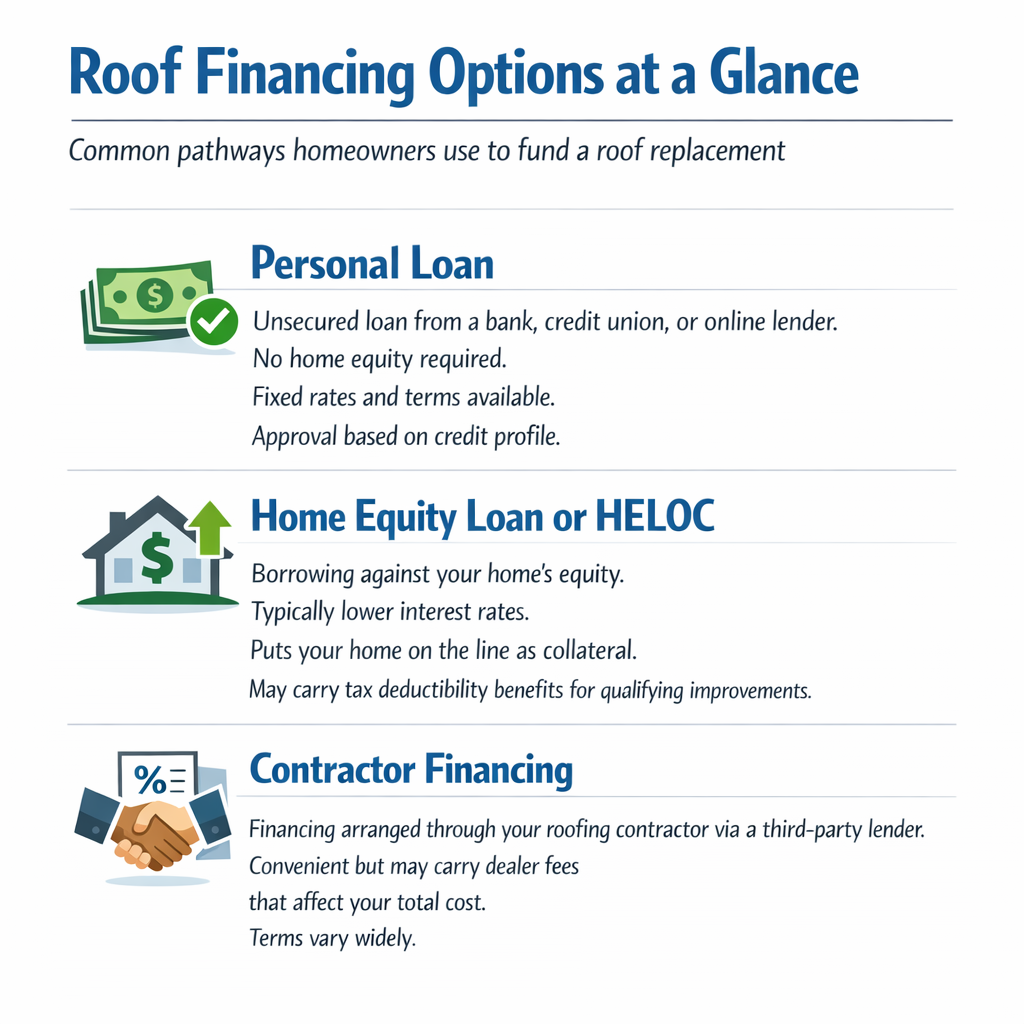

Before we get into strategy, let’s establish the landscape. Homeowners financing a roof replacement typically have access to several distinct pathways, each with real trade-offs.

(https://www.hud.gov/sites/dfiles/OCHCO/documents/17-18ml_atch.pdf)”; item4_body=”Property Assessed Clean Energy programs. Attached as a lien on your property. Repaid through property taxes. Can complicate home sales and mortgage financing.”; item5_title=”Cash-Out Refinance”; item5_body=”Refinancing your mortgage for more than you owe and using the difference. Best when rates are favorable. Folds roof cost into long-term mortgage payments.”; footer=”Smithrock Roofing — Serving the NC Triad”]

Personal loans are the most straightforward option for many homeowners. They’re unsecured — meaning your home isn’t used as collateral — and they come with fixed interest rates and predictable monthly payments. Approval is based primarily on your credit profile, income, and debt-to-income ratio.

The appeal is speed and simplicity. You apply, get approved, and the funds arrive without the home appraisal process that equity-based products require. The trade-off is that unsecured loans typically carry higher interest rates than equity-backed products, because the lender is taking on more risk.

One detail that rarely gets discussed: pay attention to whether a personal loan uses simple interest or precomputed interest. With a simple interest loan, your interest accrues on the outstanding balance — so making extra payments or paying the loan off early genuinely reduces your total interest cost. With a precomputed interest loan, the interest is calculated upfront and built into the payment schedule. The stated rate might look similar, but the true cost of capital can be meaningfully higher if you pay the loan off ahead of schedule. Always ask the lender directly how interest is calculated and what early payoff looks like.

If you’ve built equity in your home, borrowing against it is often the lowest-rate option available. A home equity loan gives you a lump sum at a fixed rate; a HELOC works more like a revolving line of credit with a variable rate.

A note on tax treatment: you may have heard that home equity interest is tax-deductible. That was broadly true before the 2017 Tax Cuts and Jobs Act, which significantly narrowed the rules. Under current law, interest on home equity debt is only deductible when the funds are used to “buy, build, or substantially improve” the home securing the loan. A roof replacement on your primary residence would likely qualify, but the specifics depend on your individual tax situation. We’d strongly encourage you to speak with a tax professional rather than assuming deductibility — what applies to your neighbor may not apply to you.

The other consideration: these products put your home on the line. If your financial situation changes and payments become difficult, a home equity product carries consequences that a personal loan does not.

This is the financing pathway that most homeowners encounter first, and it’s also the least examined in the general content out there. When a roofing contractor offers to set you up with financing at the same time they’re presenting your project estimate, two significant things are happening simultaneously: you’re evaluating the project scope and negotiating the financing terms — whether or not you realize it.

Contractor financing is arranged through third-party lending partners, and many of those arrangements involve what are called dealer fees — a cost the lender charges the contractor for originating the loan through their program. Contractors handle this in different ways. Some absorb it; others build it into the project price. The net result is that “convenient” financing arranged at the point of sale can sometimes cost more in total than financing you secured independently before the conversation started.

That said, contractor financing programs vary widely, and some are genuinely competitive. The key is knowing this dynamic exists before you sit down at the table.

PACE (Property Assessed Clean Energy) financing gets a lot of positive attention in roofing content because it offers approval without a traditional credit check and doesn’t require home equity in the conventional sense. Repayment is added to your property tax bill, which sounds simple enough.

What often goes unsaid: PACE financing attaches a lien to your property, and in many states, this lien holds a super-priority position — meaning it gets paid before most other obligations, including your first mortgage, in a default or sale scenario. Several mortgage lenders have refused to fund home purchases on PACE-encumbered properties because of this structure. If you’re planning to sell your home within the financing term, or if you anticipate refinancing, a PACE lien can create genuine complications with buyers’ lenders and your own title.

North Carolina homeowners should verify the specific terms and conditions of any PACE program available in their area and speak with both a financial advisor and their current mortgage servicer before proceeding.

If interest rates are favorable relative to your current mortgage rate — or if you were already considering refinancing — a cash-out refinance can be an efficient way to fund a roof replacement. You refinance your existing mortgage for a higher balance and receive the difference as cash.

The key strategic question here is whether the refinancing math makes sense across the full loan term. Folding a roof replacement into a 30-year mortgage means you’ll technically still be paying for it decades after the roof itself has been replaced again. This is the same logic we’ll explore in more depth when we discuss matching loan terms to material lifespans.

Here’s something no competitor content will tell you plainly: the sequence of decisions you make — financing first, or contractor first — fundamentally changes your negotiating position.

Most homeowners follow what feels like the natural path: get a few estimates, pick a contractor, then figure out financing. In practice, that sequence often means you’re evaluating financing options while already emotionally committed to a specific contractor and a specific scope of work. That’s not a position of leverage.

When you secure independent financing — or at minimum, understand your pre-approved options — before receiving contractor bids, several things shift in your favor:

The behavioral economics research on this is consistent: people make worse financial decisions when evaluating cost and credit simultaneously, especially under the time pressure that a needed roof repair creates. The simple act of separating those decisions — even by a day or two — produces better outcomes.

This isn’t a criticism of contractors who offer financing. Plenty of reputable, honest contractors work with excellent lending programs. It’s simply a reminder that you’re better off understanding your options before someone else defines them for you.

This may be the most practical piece of advice in this entire guide, and we’ve never seen another roofing website address it directly.

Every roofing material has an expected service life. Financing products have term lengths. Those two timelines interact — and when they’re mismatched, the financial consequences are real.

Consider this: if you finance a roof using an entry-level three-tab shingle that carries an expected lifespan of 15 to 20 years, and you take a loan with a 25-year term, you will still be making loan payments on that roof after it needs to be replaced. Depending on your financial situation at that future point, you may find yourself financing a second roof while still carrying the first.

Conversely, if you install a premium architectural shingle, a metal roof, or a tile system with an expected lifespan of 40 or more years, choosing a shorter loan term to “be conservative” may be unnecessarily restrictive when a longer-term product would lower your monthly payment and still close out well within the roof’s useful life.

Here’s a framework for thinking about this alignment:

| Roofing Material | Typical Lifespan | Logical Max Loan Term | Financing Consideration |

|---|---|---|---|

| Three-tab asphalt shingles | 15–20 years | 10–12 years | Avoid long-term unsecured loans; keep payoff well inside expected life |

| Architectural (dimensional) shingles | 25–30 years | 15 years | Standard personal loan or HELOC terms align well |

| Impact-resistant architectural shingles | 30+ years | 15–20 years | Consider equity products for lower rates over longer terms |

| Standing seam metal roofing | 40–70 years | 20–25 years | Long asset life supports longer financing; equity products appropriate |

| Concrete or clay tile | 50+ years | 20–25 years | Same as metal; long-term equity financing is a reasonable fit |

| Cedar shake (with maintenance) | 20–30 years | 12–15 years | Maintenance dependency adds variability; build in margin |

The principle is straightforward: your loan should be paid off before you’d reasonably need to replace the roof again. This is a financial discipline that protects you from carrying overlapping debt on the same asset.

It also has a secondary benefit: when you’re evaluating a premium material upgrade — say, moving from standard architectural shingles to an impact-resistant product — the financing lens helps clarify the real value. A material that lasts significantly longer may justify a modestly higher investment, particularly when the extended loan term keeps monthly payments manageable. For a detailed breakdown of how roofing material choices affect your total investment, the Roofing Cost Guide for NC Triad Homeowners is a useful companion resource.

At Smithrock Roofing, we install CertainTeed Landmark shingles as our standard — a premium architectural shingle backed by a limited lifetime manufacturer warranty. Understanding where that product falls on the lifespan-financing alignment table is part of how we help homeowners make decisions that hold up over time, not just on installation day.

If your roof replacement is being triggered by storm damage — hail, wind, falling trees — you’re not navigating a financing decision in isolation. You’re navigating a financing decision inside an active insurance claim, and those two processes have specific interactions that can cost you real money if you handle them independently.

Most homeowners insurance policies issue payment in two stages for roof claims. The first payment is the Actual Cash Value (ACV) — what your roof is worth today, accounting for age and depreciation. The second payment — recoverable depreciation — is withheld until the work is actually completed and documented.

This means there’s a gap. You receive partial insurance proceeds upfront, the contractor needs to be paid in full at completion, and the remaining insurance money arrives afterward. Many homeowners use short-term financing to bridge this gap — not to fund the full project, but to cover the difference between the initial payment and the contractor’s invoice until the insurance company releases the depreciation holdback.

If you apply for a loan to cover the entire roof replacement without accounting for the incoming insurance proceeds, you may end up over-borrowing — taking on more debt than you actually need once the full claim settles. Understanding this timing issue before you apply can significantly reduce your financing burden.

For a step-by-step walkthrough of how to navigate the claims process without costly missteps, Don’t Get Ripped Off: The Essential Steps for Your Roof Insurance Claim covers the full sequence in detail.

Complex insurance claims — particularly hail damage claims where the full scope of damage requires detailed contractor documentation — often go through a supplement cycle: a back-and-forth between your contractor and the insurance adjuster to agree on the full scope and approved replacement cost.

This process takes time. In some cases, several weeks or even months pass between the initial adjuster inspection and a final approved claim value. If you’ve already locked into a financing product with an early disbursement, you may be carrying loan costs during a period when you’re still waiting on the insurance to settle.

The practical advice here: if you’re in an active claim, communicate with your contractor about realistic claim timeline expectations before deciding when and how much financing to deploy.

If you carry a mortgage, your insurance company is almost certainly required to list your lender as a co-payee on any significant insurance payout. That means the check for your roof replacement doesn’t just go to you — it goes to you and your mortgage servicer, and your servicer has to endorse it before you can access the funds.

Every mortgage servicer handles this differently. Some release the funds quickly with basic documentation of project completion. Others require inspections, draw schedules, and multiple rounds of paperwork — a process that can delay your ability to pay your contractor.

This is a three-party transaction that no generic roofing financing guide acknowledges. If you have a mortgage and a storm-damage claim, call your mortgage servicer early in the process to understand their specific requirements. Your contractor should be familiar with this process as well. At Smithrock Roofing, we work with homeowners through the full insurance and payment process — it’s part of how we keep projects moving without surprises.

Most financing content treats credit as a fixed input: you have good credit, you get good rates; you have challenged credit, here are the alternative products. That’s an oversimplification that can lead homeowners to make premature financing decisions.

Your credit position at the moment you apply is what matters — and for many homeowners, a few deliberate steps taken before applying can meaningfully improve that position.

For homeowners whose credit profile has genuine challenges, the answer isn’t automatically a high-cost alternative product. It may be a matter of timing, co-borrower structure, or working with a local credit union that applies more flexible underwriting standards than large national lenders.

Homeowners in Winston-Salem, Greensboro, High Point, Kernersville, Clemmons, Rural Hall, King, and the surrounding communities face a specific roofing context worth keeping in mind as you think about financing decisions.

Our region sits in a zone that sees meaningful hail and wind activity, particularly in the spring severe weather season. That means storm-damage claims are a recurring reality here — not a rare exception. The insurance-financing interaction issues we covered above are directly relevant to what Triad homeowners navigate every few years.

Additionally, the NC housing market in our area has seen sustained value appreciation, which has meaningful implications for home equity-based financing. Many homeowners who purchased here several years ago have more equity available than they may realize — making HELOC or home equity loan options more accessible than they might assume.

Understanding your specific equity position, your mortgage servicer’s claim procedures, and the realistic weather risk profile of your home are all part of making a genuinely informed roof financing decision — not just picking the product with the fastest approval.

The best financial outcome for a roof replacement comes from working with a contractor who understands more than installation. That means someone who can discuss material lifespans honestly, walk you through the insurance claim process without confusion, and give you the project timeline information you need to make smart financing decisions.

At Smithrock Roofing, our team brings over 60 combined years of experience to every project, and we’re CertainTeed PREMIER ShingleMaster Certified — credentials that reflect genuine investment in doing this work at a high standard. We back our installations with a 5-year labor warranty on top of the limited lifetime manufacturer warranty that comes with CertainTeed Landmark shingles.

We serve homeowners across the NC Triad and surrounding communities, and we’ve worked through enough insurance claims, material upgrades, and complex projects to know that the financing conversation matters as much as the installation plan. If you’re getting ready to make a roofing decision and want a straightforward conversation about what your options actually look like, we’re ready to have it.

For a deeper understanding of roofing materials and what affects their longevity, the Insurance Institute for Business & Home Safety (IBHS) publishes independent research on roofing performance under severe weather conditions — a useful reference point for any homeowner evaluating material choices. For general guidance on comparing loan products and understanding your rights as a borrower, the Consumer Financial Protection Bureau (CFPB) offers plain-language resources that are worth reviewing before you apply for any home improvement financing.

As roofing materials, financing products, and climate conditions continue to evolve, homeowners heading into a roof replacement decision in 2026 are better served by preparation than by speed. Three specific steps can meaningfully improve your outcome before you sign anything.

1. Request a Formal Roof Condition Report Before Applying for Financing

Rather than estimating your financing need based on a verbal quote alone, ask your contractor for a written scope-of-work document that details material specifications, projected labor timeline, and any identified structural concerns. This documentation gives you a concrete basis for comparing loan products and helps you avoid under-borrowing or over-borrowing for your actual project.

2. Pull Your Insurance Declarations Page and Review It Annually

Many homeowners don’t review their homeowner’s insurance policy until they need to file a claim — and that’s when they discover gaps in coverage. Before your roofing project begins, locate your declarations page, confirm your dwelling coverage limits, and check whether your policy pays actual cash value or replacement cost value. That single distinction can significantly affect how much out-of-pocket financing you actually need.

3. Use the CFPB’s Loan Comparison Tools Before You Commit

The Consumer Financial Protection Bureau offers free, plain-language tools for comparing loan types and understanding the total cost of borrowing over time. Before accepting any financing offer from a contractor, lender, or bank, spend time with these tools. Understanding the difference between promotional terms and standard terms — and what happens if those terms change — is foundational knowledge for any borrowing decision.

Homeowners generally have several paths available: personal home improvement loans through banks or credit unions, contractor-facilitated financing through third-party lenders, home equity loans or lines of credit, and in some cases manufacturer-affiliated financing programs. Each option carries different term structures, interest rates, and qualification requirements. The right choice depends on your credit profile, how long you plan to stay in the home, and whether your project timeline is urgent or flexible.

This depends on the cause of the damage and the age of your roof. If deterioration is weather-related — storm damage, hail impact, or wind uplift — filing an insurance claim is often the appropriate first step. If the damage is primarily due to age or deferred maintenance, your insurer may not cover replacement. A contractor experienced in insurance claims can help you assess which path makes more sense before you commit to either approach.

Material selection affects both the upfront scope of your financing need and the long-term value of what you’re financing. Longer-lifespan materials may carry a higher initial cost but reduce the likelihood of another replacement within your ownership window. Some materials also qualify for insurance discounts or impact-resistant ratings that can affect your ongoing carrying costs as a homeowner — which indirectly influences the overall financial picture of any loan you take on.

Look for verifiable credentials, transparent documentation, and a willingness to explain the full project scope in writing. Certifications like CertainTeed PREMIER ShingleMaster reflect a contractor’s investment in installation standards, not just sales volume. Ask about labor warranty terms separate from manufacturer warranties, confirm the contractor is licensed and insured in your state, and make sure they can walk you through the insurance claim process if that’s relevant to your project — before financing enters the conversation.

Homeowners in Winston-Salem and Greensboro deserve a roofing partner who brings both technical expertise and honest guidance to one of the more significant decisions you’ll make as a property owner. Smithrock Roofing’s combination of CertainTeed PREMIER ShingleMaster Certification, over 60 combined years of field experience, and deep familiarity with the NC Triad’s climate and insurance landscape means you’re working with a team that understands what’s actually at stake. When you’re ready to talk through your options without pressure, Get a Free Estimate and we’ll start with the conversation that actually helps you move forward.

Smithrock Roofing © Copyright 2026 • All Rights Reserved • Privacy Policy • Maintained by Mongoose Digital Marketing