Filing a roof insurance claim after a hailstorm rolls through Greensboro or a wind event strips shingles off a home in Kernersville should feel straightforward. You paid your premiums. Something damaged your roof. Your insurer should cover it.

In practice, the gap between what homeowners expect and what they actually receive on a settlement check is often significant — and it has nothing to do with whether the damage is real or the coverage is legitimate. It has everything to do with a process most homeowners enter completely unprepared.

This guide exists to change that. We’re going to cover what every other article covers — yes, we’ll walk through the basics of what’s covered and how to file — but we’re also going to go deeper into the parts that actually determine whether your claim succeeds or stalls. Who the adjuster is, how estimates are calculated, what “recoverable depreciation” really means for your wallet, and what to do if your claim gets denied. These are the details that matter most, and they’re the ones most homeowners only learn after the fact.

If you’re a homeowner in Winston-Salem, High Point, Clemmons, King, Rural Hall, or anywhere across the NC Triad, this is the honest, experience-backed walkthrough you deserve before you pick up the phone and dial your insurance company.

Before you file anything, it’s worth understanding what triggers a covered claim versus what your insurer will decline — often citing policy language buried in your declarations page.

Standard homeowners insurance policies in North Carolina cover what’s called “sudden and accidental” damage. The most common covered causes include:

Understanding this distinction early prevents the frustrating experience of filing a claim, waiting through the inspection process, and receiving a denial that was predictable from the start.

Every competitor article explains this distinction, and for good reason — it’s foundational. But most explanations stop short of the detail that actually matters to your bank account.

Actual Cash Value (ACV) pays you what your roof is worth today, accounting for its age and depreciation. If your 15-year-old roof has a useful life of 25 years, you’ve already “used” roughly 60% of it. An ACV policy will only pay the remaining 40% of the replacement cost after your deductible.

Replacement Cost Value (RCV) pays the actual cost to replace your roof with materials of similar kind and quality — without the depreciation haircut.

RCV policies don’t pay out everything at once. Here’s how the process actually works:

That second payment is not automatic. And it has a deadline.

Most policies require you to submit proof of completed repairs within 180 days to two years of the initial claim payment, depending on your specific policy language. Homeowners who delay repairs — or who complete the work but forget to submit the documentation — permanently forfeit that second check. It’s one of the most preventable ways legitimate claim money goes uncollected.

Before repairs begin, ask your contractor to confirm they will provide you with all three of the following:

| Document | Purpose | Who Provides It |

|---|---|---|

| Final contractor invoice | Proves the full scope of work was completed | Your roofing contractor |

| Certificate of completion | Formal confirmation work is finished | Your roofing contractor |

| Permit inspection sign-off | Required in jurisdictions where a permit was pulled | Local building department |

Missing even one of these can delay or block the depreciation release. Make sure you understand what your specific policy requires before your contractor leaves the job site.

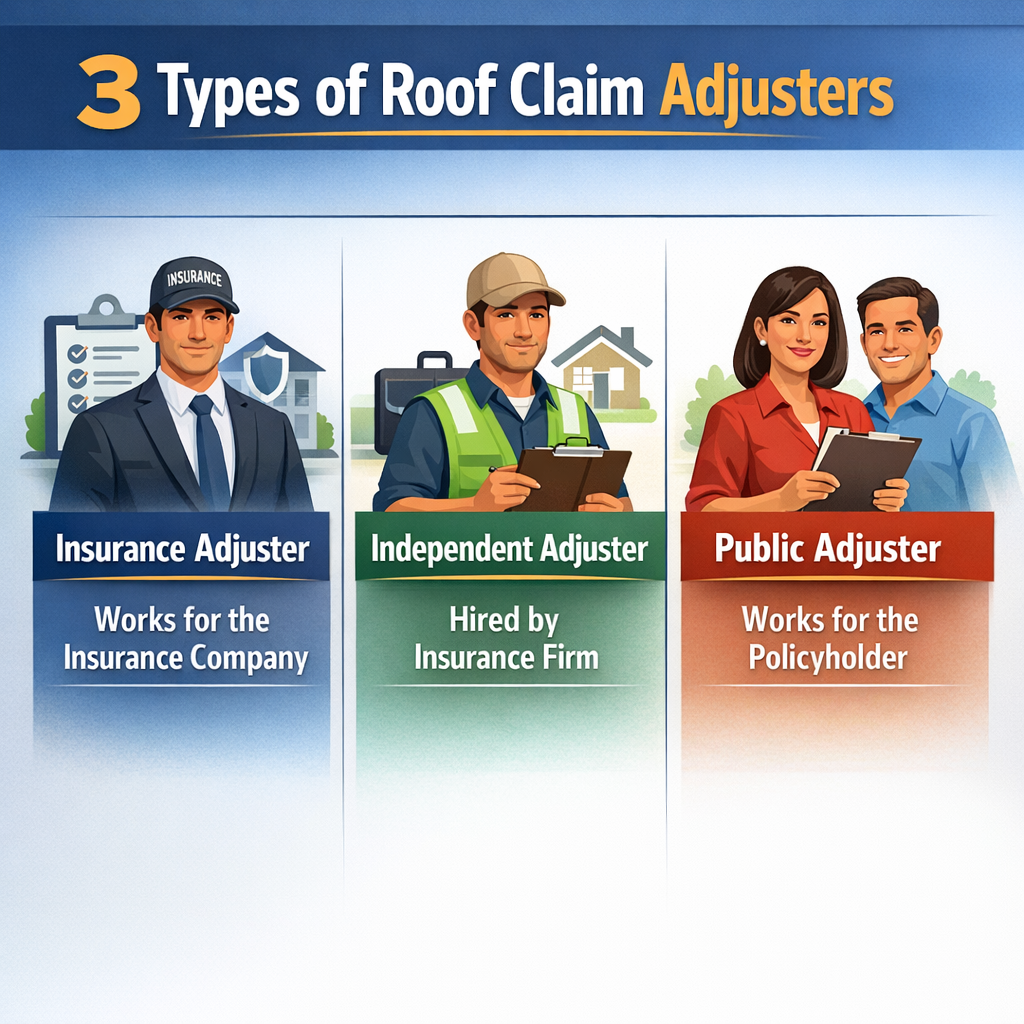

This is the part of the roof insurance claim process that almost no one explains clearly, and it’s arguably the most consequential variable in your final settlement.

When your insurer sends someone to inspect your roof, that person falls into one of three categories — and understanding which one changes how you should prepare for that visit.

Staff adjusters are direct employees of your insurance company. They draw a salary, receive benefits, and are evaluated on performance metrics that typically include claim closure speed and reserve management. This doesn’t mean they’re dishonest — most are professional and thorough — but their institutional incentives are not aligned with maximizing your payout. They represent the insurer.

Independent adjusters are contracted third parties. Insurance companies lean on them heavily after large regional storm events — the kind that sweep across the NC Triad and generate hundreds of simultaneous claims. When staff adjusters are overwhelmed, independents are deployed to close the backlog. Their workload during catastrophe events can be intense, and the quality and thoroughness of their inspections varies meaningfully from one individual to the next.

A public adjuster is the only person in this entire process who is explicitly working on your behalf. Homeowners hire them directly, and they’re compensated on a percentage of the final settlement amount — which means their financial incentive is entirely aligned with documenting as much legitimate damage as possible.

The practical takeaway: When you receive notice that an adjuster will be visiting, ask your insurer whether they’re sending a staff adjuster or an independent adjuster. That single question gives you meaningful information about whether engaging a public adjuster or simply having your contractor present during the inspection would be worth the effort — decisions that are far harder to reverse after a low settlement offer arrives.

Here’s something the major insurance carrier websites will never tell you: the number on your settlement offer wasn’t hand-calculated by your adjuster. It was generated by software.

The vast majority of U.S. insurers and adjusters use a platform called Xactimate to build repair cost estimates. It’s a line-item estimating tool that draws on regional pricing databases for labor and materials.

The catch? Those databases update on a schedule, not in real time. In the aftermath of a major storm event — when every roofing contractor across the Triad is booked out and material demand has pushed prices up — the Xactimate pricing database may still be reflecting pre-storm market conditions. The result is a settlement offer that looks legitimate on paper but doesn’t reflect what it actually costs to complete the work in today’s market.

A roofing contractor who is Xactimate-certified can submit a competing line-item estimate in the exact same format that insurers and adjusters use. That’s a fundamentally different conversation than presenting a general quote on company letterhead.

When a contractor hands an adjuster or claims supervisor a properly formatted Xactimate counter-estimate with documented line items — including material waste factors, regional labor rates, and permit costs — it carries weight that informal quotes simply don’t. It speaks the insurance industry’s language, and it gives the insurer a specific, documented basis for revisiting a low initial offer.

This surprises most homeowners: depreciation figures on a roof claim are not standardized. Different insurers use proprietary depreciation schedules, and the same 12-year-old roof can receive materially different depreciation rates depending on who carries the policy.

More importantly, those figures can be challenged.

When a contractor conducts a thorough damage assessment and submits supplemental documentation — including material cost comparisons, regional pricing evidence, and line-item justifications — depreciation calculations become a negotiation, not a final verdict. This process is called claim supplementing, and it’s standard practice among experienced roofing contractors who handle complex claims regularly.

Supplementing isn’t about inflating a claim. It’s about ensuring the documented scope of work reflects the actual damage found — including damage that wasn’t visible during the initial adjuster inspection, which is common after hail impacts that damage structural components beneath the surface. For a deeper look at what those hidden impacts actually look like, the article Hail Damage Roof Repair: What You Can’t See walks through what adjusters often miss and why it matters to your claim.

Here’s a scenario that plays out regularly across North Carolina: a storm damages one side of your roof. The adjuster documents that slope, and the insurer offers to replace only the affected section.

The problem? Your shingles are a discontinued color that’s no longer manufactured. Replacing half your roof creates a permanent two-tone appearance that affects both curb appeal and resale value.

Many states recognize what’s called the matching rule — the principle that when partial roof damage occurs and matching materials are unavailable, the insurer may be required to replace the full contiguous roof surface to restore the home to a uniform appearance. This principle has been the subject of active litigation across multiple states, and its application in North Carolina depends on your policy language and the specific circumstances of the damage.

This isn’t a claim inflation tactic. It’s a consumer protection concept rooted in the fundamental purpose of property insurance: to restore your home to its pre-loss condition. An experienced roofing contractor who works with insurance claims regularly will know whether this applies to your situation and how to document it properly if it does.

After a significant weather event crosses the Triad, out-of-town contractors begin appearing in neighborhoods within days — sometimes hours. They knock on doors, offer free inspections, and create urgency around signing paperwork before you’ve had a chance to think clearly.

Most homeowners know to be cautious. But the specific mechanism that makes these situations genuinely dangerous goes beyond shoddy workmanship.

Some storm-chasing contractors will present a document called an Assignment of Benefits (AOB) — sometimes embedded in what appears to be a standard work authorization form. When you sign an AOB, you are legally transferring your claim rights to the contractor. That means the contractor can negotiate your claim, accept a settlement, and even pursue legal action against your insurer — all without your direct involvement or approval.

In several states, this has created significant consumer protection concerns. Once your claim rights are assigned, you lose meaningful control over the outcome of your own claim.

Before signing anything from a contractor after storm damage, confirm:

Working with a contractor who has deep roots in the NC Triad — one with an established reputation, verifiable reviews, and a track record of standing behind their work long after the truck leaves your driveway — is your single best protection against this scenario. If you’re not sure what credentials and track record actually look like in practice, the article How to Choose the Best Roofing Contractor in Winston-Salem, NC (And What Credentials Actually Matter) walks through exactly what to look for before you commit.

Here’s a coverage gap that surprises even financially savvy homeowners.

Older homes in established neighborhoods — the kind found throughout High Point, Winston-Salem’s historic districts, and older Greensboro subdivisions — were built to building codes that have since been updated. When a covered loss triggers a full or partial roof replacement, local building departments may require the work to meet current code standards, not the standards that existed when the home was built.

Without Ordinance or Law coverage (also called building code coverage) as a policy endorsement, those upgrade costs fall entirely on the homeowner — even on an otherwise fully covered claim. This can mean upgraded decking, revised ventilation systems, ice and water shield requirements, or updated flashing standards, depending on what local code requires.

Check your policy’s declarations page for this endorsement. If it’s not there, it’s worth a conversation with your insurance agent before the next storm season arrives — not after.

The roof insurance claim process has multiple overlapping timelines, and confusing them is a costly mistake.

| Deadline Type | What It Is | Typical Timeframe |

|---|---|---|

| Policy reporting deadline | How quickly after a loss you must notify your insurer | Often 30–60 days, varies by policy |

| Proof of loss submission | Formal sworn statement of loss and documentation | Often 60 days post-claim filing |

| Recoverable depreciation window | Deadline to submit repair completion docs for RCV release | Typically 180 days to 2 years |

| State statute of limitations | Legal window to file a lawsuit over a disputed claim | 3–5 years in NC, depending on circumstances |

| Policy renewal and re-inspection | Some insurers re-inspect after a claim; undocumented prior damage can affect future coverage | Varies |

These are distinct deadlines governed by different sources — your policy contract, state insurance regulations, and civil law. Missing the proof of loss deadline, in particular, can compromise an otherwise legitimate claim even if you’re well within the state’s statute of limitations.

When in doubt, move faster rather than slower. Document early, notify your insurer promptly, and keep a written record of every communication — date, time, representative name, and a summary of what was discussed.

A denial letter is not the final word. It is, in many cases, a starting point.

When you receive a denial, the sequence of options available to you — in order of escalation — typically looks like this:

Written appeal with supplemental contractor documentation — Submit a formal written appeal that includes your contractor’s line-item damage assessment, photos with timestamps and context, and any relevant building code considerations. Many denials are reversed at this stage when the supporting documentation is thorough.

State insurance department complaint — The North Carolina Department of Insurance handles consumer complaints against insurers and has the authority to investigate whether a claim was handled in accordance with state regulations. Filing a complaint costs nothing and creates an official record.

Appraisal clause invocation — Most homeowners policies include an appraisal clause that allows both parties to appoint their own independent appraiser when there’s a dispute over the amount (not the coverage) of a loss. This is a faster, less expensive alternative to litigation and is worth understanding before you hire an attorney.

Litigation — If the above steps are exhausted or the insurer’s conduct rises to the level of bad faith, legal action is an option. Consult with an attorney who specializes in insurance claims in North Carolina.

The passive framing you’ll find in most articles — “you may have the right to appeal” — undersells this significantly. Understanding the specific tools available to you, in sequence, is what separates homeowners who recover their full entitled settlement from those who accept an insufficient offer because they didn’t know there was anything else to do.

Every guide tells you to “take photos.” That advice, without context, isn’t very useful.

Here is what systematic documentation actually means in the context of a roof insurance claim:

Adjusters are trained to evaluate the quality and completeness of photo evidence. Homeowners who submit a thorough, organized documentation package are treated differently — and more favorably — than those who submit a handful of casual snapshots.

Not all roofing contractors are equally equipped to help you through a roof insurance claim. Some are excellent at installation but have limited experience with the documentation, supplementing, and negotiation side of the process. Others — particularly out-of-town storm chasers — know the insurance side very well but have no long-term accountability to the homeowner.

The contractor you want is the one who knows both: the technical side of the work and the process of working alongside insurance carriers to ensure the documented scope reflects the actual damage.

At Smithrock Roofing, we’ve helped homeowners across the NC Triad navigate exactly this process — from the initial inspection through final settlement. Our team is familiar with how adjusters evaluate damage, how Xactimate estimates are structured, and how to document supplemental line items in a format that carries weight with insurance claims departments. We’re also CertainTeed PREMIER ShingleMark Master Certified, which means the materials we install and the workmanship we deliver meet a standard that supports — not undermines — the investment your insurance claim is designed to protect. You can learn more about our roofing services and what sets our approach apart.

If you’re dealing with storm damage to your roof in Winston-Salem, Greensboro, High Point, Kernersville, Clemmons, Rural Hall, King, or anywhere nearby, we’re glad to start with an honest inspection and a straight answer about what we see.

As roof insurance claims become more documentation-intensive and carriers continue tightening their evaluation criteria, homeowners in the NC Triad can position themselves more effectively by taking a few proactive steps before damage ever occurs.

1. Schedule an Annual Roof Inspection and Request a Written Report

A dated, written inspection report from a qualified roofing contractor creates a clear pre-loss baseline. If damage occurs later — from a hailstorm, high winds, or a falling tree — that report becomes one of the most useful documents you can hand to an adjuster. It demonstrates the roof’s condition before the event and removes any ambiguity about whether damage is new or pre-existing. Scheduling this annually, ideally in late spring or early fall, keeps your documentation current.

2. Use a Weather Event Tracking App or Service

Tools like the National Weather Service storm archive, Weather Underground’s historical data lookup, or insurance-focused apps designed for homeowners can help you log significant weather events tied to your address. In 2026, several of these platforms allow users to pull documented wind speed, hail size, and storm path data for a specific location and date — exactly the kind of third-party corroboration that supports a roof insurance claim when an adjuster questions whether a qualifying event occurred.

3. Build a Home Maintenance File Before You Need It

A simple digital folder — stored in cloud backup — containing dated photos of your roof, receipts from past repairs, warranty documents, and any contractor correspondence gives you a ready-made documentation package when a claim becomes necessary. Homeowners who can produce organized records move through the claims process faster and with fewer disputes. Start the folder now, update it after any roof work or inspection, and treat it the same way you’d treat records for your HVAC system or major appliances.

Most homeowner insurance policies cover sudden, accidental damage caused by specific events — hail, wind, falling trees, and similar perils. Damage from age, wear, or deferred maintenance is typically excluded. The most reliable way to find out whether your situation qualifies is to have a contractor with insurance claims experience inspect the roof before you file. They can identify whether the damage pattern is consistent with a covered event and help you understand what an adjuster is likely to see.

This is more common than most homeowners expect, and it doesn’t mean the process is over. If your contractor identifies line items that were missed or undervalued in the adjuster’s estimate, a formal supplement can be submitted with documentation supporting those additions. Having a contractor who is familiar with how estimates are structured — and who can communicate in the same format adjusters use — makes this process significantly more straightforward.

Rate impacts vary by carrier, policy type, claims history, and state regulations. In some cases, a single weather-related claim has no effect on premiums. In others, it may be a factor at renewal. This is a question worth asking your insurance agent directly before you file, so you can weigh your options with complete information. What’s generally consistent is that legitimate damage from a covered event is exactly what insurance is designed for.

The timeline depends on several factors — how quickly the adjuster is assigned, whether the scope is agreed upon immediately or requires supplementing, the carrier’s internal processing time, and material availability on the contractor’s end. Simple claims with clear documentation and no disputes can move relatively quickly. Claims that require supplemental submissions or involve more complex damage may take longer. Staying organized and responsive throughout the process — and working with a contractor who communicates clearly with your carrier — helps avoid unnecessary delays.

Navigating a roof insurance claim takes preparation, documentation, and a contractor who understands both the technical and administrative sides of the process — and that’s exactly what homeowners in Winston-Salem and Greensboro have come to expect from Smithrock Roofing. Whether the storm rolled through last week or you’ve been sitting on unaddressed damage and aren’t sure where to start, our team is ready to give you a straight answer and a clear path forward. Get a Free Estimate and let’s take a look at what’s going on up there.

Smithrock Roofing © Copyright 2026 • All Rights Reserved • Privacy Policy • Maintained by Mongoose Digital Marketing